Uncertainty Seems Certain -- Factors at Play for M&A

Uncertainty Seems Certain -- Factors at Play for M&A

Panther Equity Insights -- a private equity newsletter covering all things IT & Telecom, Tech & Business Services, eCommerce and Markets.

Welcome to another edition of Panther Equity Insights! Whether you are a business owner, current or potential investor, or operate within the IT & Telecom Services, Technology Services, Business Services, or eCommerce sectors, we are delighted to have you with us.

This week we’re looking at:

Elevated LOI Breakage Rates in LMM M&A

How The Cost of Debt is Starting to Impact “Buy & Build” Opportunities (aka Roll-Ups)

Industry Commentary from Fellow Operators and Investors

Our aim is to provide you with valuable insights, reports, firm updates, and thought leadership on the latest trends and advancements in these verticals. We strive to create a newsletter that is easy to read, thought-provoking, and entertaining.

We’re Looking For Deals 🎯

Our team is focused on making investments within the IT & Telecom Services, Technology Services, Business Services & eCommerce verticals. Along with our operating partners, we have decades of experience within the mentioned verticals paired with a vast network of experienced operators and LP investors.

If you’re a Founder / Shareholder interested in working with Panther, or an intermediary with a deal to share — feel free to reach out and get in touch with us! We are happy to compensate fees to intermediaries & referrals at market levels.

Private Market Movements

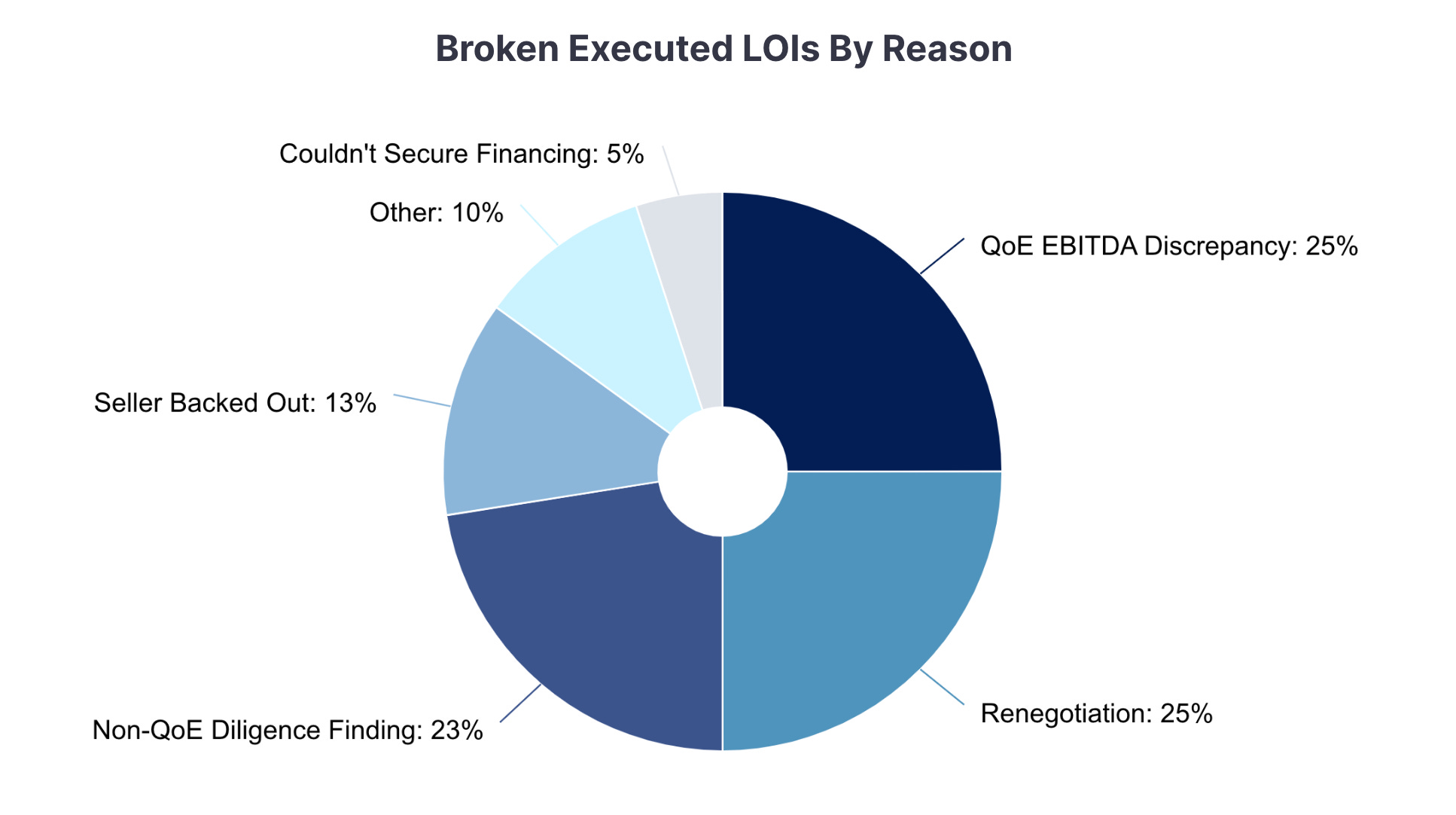

Elevated LOI Breakage Rates: A Common Theme for 2022

A recent Axial survey polled M&A players (PE, Investment Bankers, Intermediaries, etc.) and uncovered a few reasons behind the rise in failed LOIs in 2022 (disclosure — Panther was a respondent for 2 deals in this survey for 2022; (1st) Seller Backed out and (2nd) Rising interest rates impacting capital structure tolerance (“Other”)). Despite challenging macroeconomic conditions & uncertainty, debt financing issues were not identified as the primary cause by the respondents. Rather, the survey indicated a combination of “Seller Financial Unpreparedness” and “Unsuccessful Renegotiations following Due Diligence” were the main factors leading to the failure of LOIs.

How does Panther think through this?

We continue to stay in industries we know, love, and have Operating Relationships in. Since we are industry-specialized investors, we will ‘spot’ diligence hair / complexity weeks or month(s) before ‘LOI stage’ via industry knowledge and relationships. This is by design as it allows us to properly call out ‘troubled areas’ up-front and creatively think through a bridgeable solution with company management via deal-structuring or post-closing operational initiatives.

As a reminder — Panther Equity Group has ample capital + LP relationships excited to make investments in 2023. If you are a company shareholder, deal intermediary, or advisor with a company that could be interested in a transaction (minority recapitalization, majority exit, or growth equity) in 2023, feel free to reach out!

Here’s an overview of our investment criteria ⬇️

Our Preferred Investment Criteria 🎯

Industry focus: IT & Telecom, Business Services, and eCommerce

Size: EBITDA of $2 million – $12 million / $10M to $100M enterprise value

Geography: U.S. or Canada headquarters

Target Transaction: Majority, significant minority, and structured equity investments

Business Profile: Founder or closely-held ownership with an experienced management team

Industry Commentary

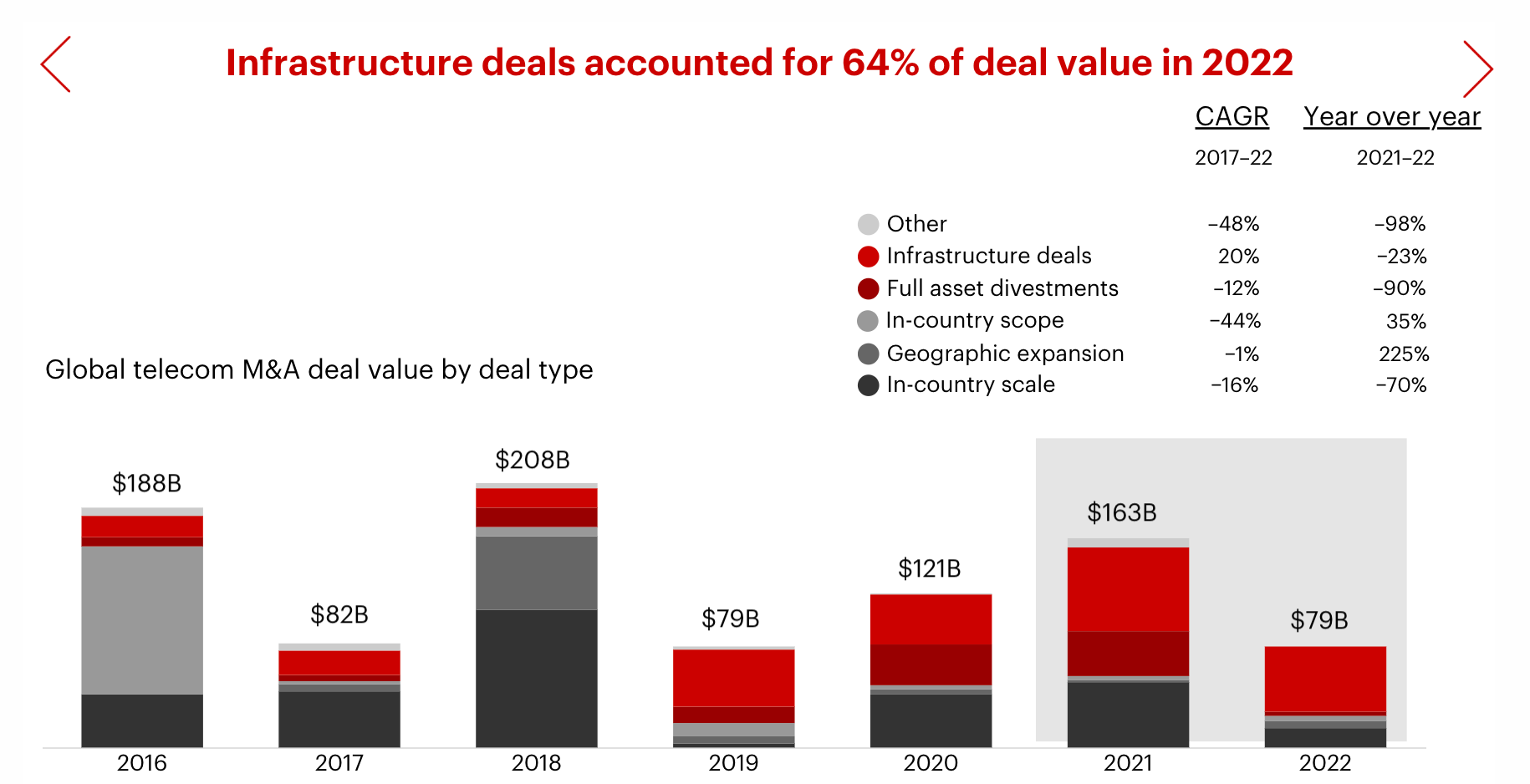

Telecom

Infrastructure deals made up about 64% of global deal value, primarily due to a spate of tower deals totaling around $32 billion. Infrastructure deals accounted for a whopping 96% of total deal value in the fourth quarter alone.

Private Equity

The aggregator theory is in full effect, as GPs deploy capital and seek to raise successor funds at shorter intervals.

eCommerce

The Fortia Group is an M&A firm focused exclusively on eCommerce exits. Their Exit Guide is a great resource for founders and operators in the DTC space.

CFO Insights

Broader Market Chatter

Cost of Debt is Impacting Buy & Build / Roll-Up Opportunities (**especially those with minimal organic growth**)

Our team recently shared insights on the impact of raising rates as it pertains to investors:

Amongst investors, there is a clear focus of attention on the impact that rising interest rates will have on the deal-making environment. In a more risk-averse environment, debt financing will be harder to come by, especially at the upper end of the market. This already occurred as the bank leveraged loan market essentially dried up in Q4’2022. Many banks have transitioned into ‘risk-off’ mode and retreated from funding leveraged buyouts.

But the second and third-order consequences of raising rates are currently being felt across industries. According to a Bain report, relying on add-on opportunities for a platform when there are a) migrant demographics of customers, b) government budget pressures, c) shifting material + labor cost elements, and d) rising interest rates — the blueprint model of acquiring a Platform (i.e., TargetCo) with goal of acquiring 3-10+ regional competitors (i.e., add-ons) has been extremely successful by PE firms in a low-interest rate environment.

Today, however, unless the investor(s) is willing to continue funding M&A with strong levels of equity, there is a higher risk that add-on integration could not be extremely margin-accretive or revenue-impacting in certain businesses. Integration creates additional ‘operational complexity’ that many management teams in the lower middle market do not have experience in and can also cause revenue attrition (churn / loss) via distractions on integration vs core business focus.

Additionally, a large benefit of Buy & Builds / Roll-Ups historically has been due to ‘multiple arbitrage’ where you buy in at a multiple that is lower than the multiple you exit at down the road. Today it is difficult to predict with confidence how multiples will change over the next 3-7 years of an investment period for a company (due to interest rate movement).

Although for some opportunities & management teams, the Buy & Build may work, there is good reason for extreme caution and reassessment of which verticals, business models, and teams are best to continue this strategy — especially with more debt in the mix being layered on after each acquisition.

How does Panther think through this?

We look to win in this environment through investments that are exciting to us, management teams, and investors via “organic growth underwriting” upon initial reviews.

This means simply —> if the opportunity at hand does not work ‘without additional M&A’, we pass. We work hand-in-hand with our Operating Partners + Company Founders / Management to formulate organic thesis via (i) Services / Product Growth, (ii) End-Customer Market Expansion, (iii) Geographic Growth, (iv) Automation & Tech Enablement, (v) Middle Management Development / Hiring, (vi) Sales / Marketing Initiatives, (vii) Professionalization and more.

If Panther & our team believe a thesis can be a home-run ‘organically’ and ‘add-on M&A’ can further enhance — we certainly remain excited to explore.

Panther Equity Insights <> Deal Bridge Media

This newsletter was powered by the team at Deal Bridge Media. Deal Bridge builds newsletters for M&A firms to help them generate more inbound deal flow.

Does your investment firm want to start a newsletter? Get in touch with Deal Bridge today!

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.