Telecom M&A Faces Strong Macro Headwinds

Panther Equity Insights -- a private equity newsletter covering all things IT & Telecom, Tech & Business Services, eCommerce and Markets.

Happy Wednesday folks! Welcome back to this week's edition of Panther Equity Insights, the bi-weekly newsletter from Panther Equity Group.

This week we’re looking at:

Telecom M&A Market Update: Strong Macro Headwinds

Industry Commentary on SaaS, AI, and PE

Broader Market Chatter on Cloud Investment Growth

Our aim is to provide you with valuable insights, reports, firm updates, and thought leadership on the latest trends and advancements in these verticals. We strive to create a newsletter that is easy to read, thought-provoking, and entertaining.

Before we begin, if you’re a company Founder / Shareholder interested in working with Panther, a deal maker interested in connecting or with a deal to share, or an Operating Executive looking for a part-time, full-time, or a Board Level Role — feel free to get in touch with us!

Private Market Movements

Telecom M&A Faces Strong Macro Headwinds

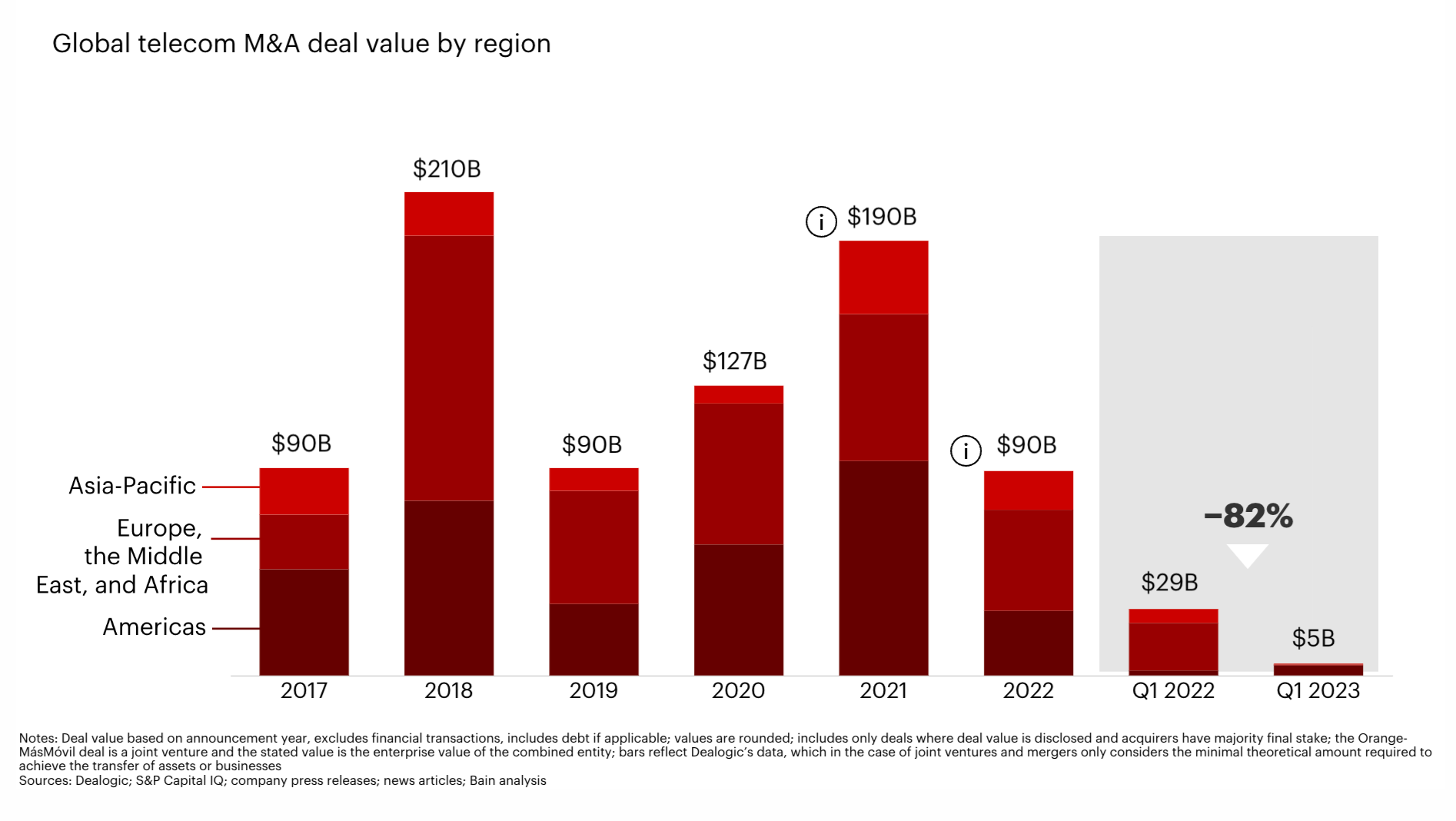

Bain’s recent Telecom M&A report shows an 82% year-over-year drop in telecom M&A deal value in the first quarter of 2023.

The main driver for the significant decline is high interest rates coupled with the verticals traditionally high leverage, harming the economics of certain deal structures. The decline reflects a continuation of 2022’s downtrend as “free money” started drying up. 2021 levels of M&A activity, fueled by near-zero interest rates and record level private equity dry powder, may not be seen in the foreseeable future.

We’ll still see deal activity in certain areas despite the current environment, especially in the Americas which comprised 85% of deal activity in Q1 2023.

Below, we’ll dig into deal types that show promise as well as industry insights for operators and dealmakers.

Infrastructure Deals Dominate

Infrastructure has drawn significant interest across private equity and pensions. Many funds are eager to add high quality telecom assets to their portfolios due to their positioning to benefit from digitalization and their highly contracted nature. As a result, digital infrastructure EV/EBITDA multiples have soared to nearly 25x by the end of 2022 compared to 2021’s 17x average.

Infrastructure funds will continue to dominate 2023 activity, already capturing 69% of deal value in Q1. Though deal economics have weakened from interest rates, funds still have record levels of dry powder and will continue deploying into digital infrastructure assets. Telecoms are happy to divest and sell to funds as multiples in the private market have skyrocketed above public valuations. It also fits the recent trend of telcos disaggregating from the integrated model to more vertical approaches. Sellers should keep in mind that revenue growth and high asset utilization are now the main factors driving recent acquisitions since acquirers can no longer realize as much value with leverage.

Implications for Middle Market Telcos

Challenger telcos will struggle once the previously cheap debt they used for growth comes up for refinancing. Bain predicts alternative networks, or “altnets”, to be especially impacted in developed fiber markets. Telcos will need to find an exit strategy as they lag on investment plans, fail to capitalize on builds, and miss milestones or covenants for their debt-financing. Once this happens, consolidation may become the only option and it could open an opportunity for middle market digital infrastructure funds to build their portfolios.

5 Questions for Telecom Players in 2023

Telcos need to understand the implications of the new environment and how it impacts their strategy. The industry remains robust despite lowered M&A and will benefit from long-term tailwinds including 5G, fiber demand, IoT, and cloud computing.

Bain highlights five critical questions all telecom players should consider for 2023:

What market consolidation options are left, and how can they be achieved via M&A?

Can we be front-runners for fiber, tower, and data center rollup and consolidation?

Which challenger telcos will be most impacted by inflation and the rising cost of debt, and how will that impact M&A action?

With the great delayering of the telecom business model underway, can infrastructure assets such as edge data centers and mobile Internet companies still be created?

Where are the undervalued, listed telco assets that could create more value as a private company?

Industry Commentary

Enterprise SaaS: After a resilient 2022, enterprise SaaS showed signs of further slowdown in Q1.

Generative AI: Harvard Business Review podcast on how the rise of generative AI changes tech business strategy.

Cloud: Survey by Aptum finds the main cloud frustrations by interviewing 400+ IT professionals across the U.S., U.K., and Canada.

Broader Market Chatter

Cloud Investment Growth Slows for the First Time as Customers Shift Focus

Worldwide cloud spending increased 19% to US$66.4 billion in Q1 2023 based on a recent report by technology analyst firm Canalys. Though cloud remains one of IT’s fastest growing segments, the Q1 figure represents the first quarter where cloud spending growth dipped below the 20% threshold. Many industries would be happy with near 20% growth rates in today’s climate, but with cloud growth rates averaging in the high 30s until now, the slowdown is definitely felt.

Enterprises are showing a clear focus on optimizing cloud spend, reducing cloud ‘waste’ and improving the efficiency of cloud deployments. As a result, the top three hypserscalers — AWS, Azure, and Google Cloud — who collectively control 64% of the market, have all announced layoffs and internal budget cuts in their respective cloud divisions. Canalys expects the cloud slowdown to continue for at least the remainder of 2023.

Opportunity for Cloud Service Providers to provide Tailored Solutions

The cloud forecast may seem gloomy, but this trend actually presents a strong opportunity for cloud service providers to advise customers on building highly customized cloud solutions. For service providers, here’s what customers are becoming increasingly interested in:

Implementing observability, FinOps and AI to optimize cloud spend

Repatriating certain workloads back on-premises using hybrid cloud

Incorporating generative AI into tech stacks

These solutions are complex and require the expertise of channel partners. Canalys predicts an outsized opportunity for hybrid cloud services as VP Alex Smith explains, “Enterprises are benefiting from the hybrid cloud model, but moving workloads between on-premises and cloud platforms can be costly for them. Increased reliance on complex cloud environments may result in challenges when it comes to managing them, but there are supporting technologies that can play a big role in identifying efficiencies and streamlining processes, especially in automating routine tasks and analytics.”

Panther Equity Insights <> Deal Bridge Media

This newsletter was powered by the team at Deal Bridge Media. Deal Bridge builds newsletters for M&A firms to help them generate more inbound deal flow.

Does your investment firm want to start a newsletter? Get in touch with Deal Bridge today!

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.