Telecom Deal Value Declines in Q3, but Opportunities Persist

Telecom Deal Value Declines in Q3, but Opportunities Persist

Panther Equity Insights -- a private equity newsletter covering all things IT & Telecom, Tech & Business Services, eCommerce and Markets.

Happy Wednesday folks! Welcome back to this week's edition of Panther Equity Insights, the bi-weekly newsletter from Panther Equity Group.

This week we’re looking at:

Telecom M&A Update from Bain

Industry Commentary on Cloud, M&A & Ai

Broader Market Chatter on Tech Target’s IT Services Trends

Our aim is to provide you with valuable insights, reports, firm updates, and thought leadership on the latest trends and advancements in these verticals. We strive to create a newsletter that is easy to read, thought-provoking, and entertaining.

Before we begin, if you’re a company Founder / Shareholder interested in working with Panther, a deal maker interested in connecting or with a deal to share, or an Operating Executive looking for a part-time, full-time, or a Board Level Role — feel free to get in touch with us!

Private Market Movements

Telecom Deal Value Declines in Q3, but Opportunities Persist

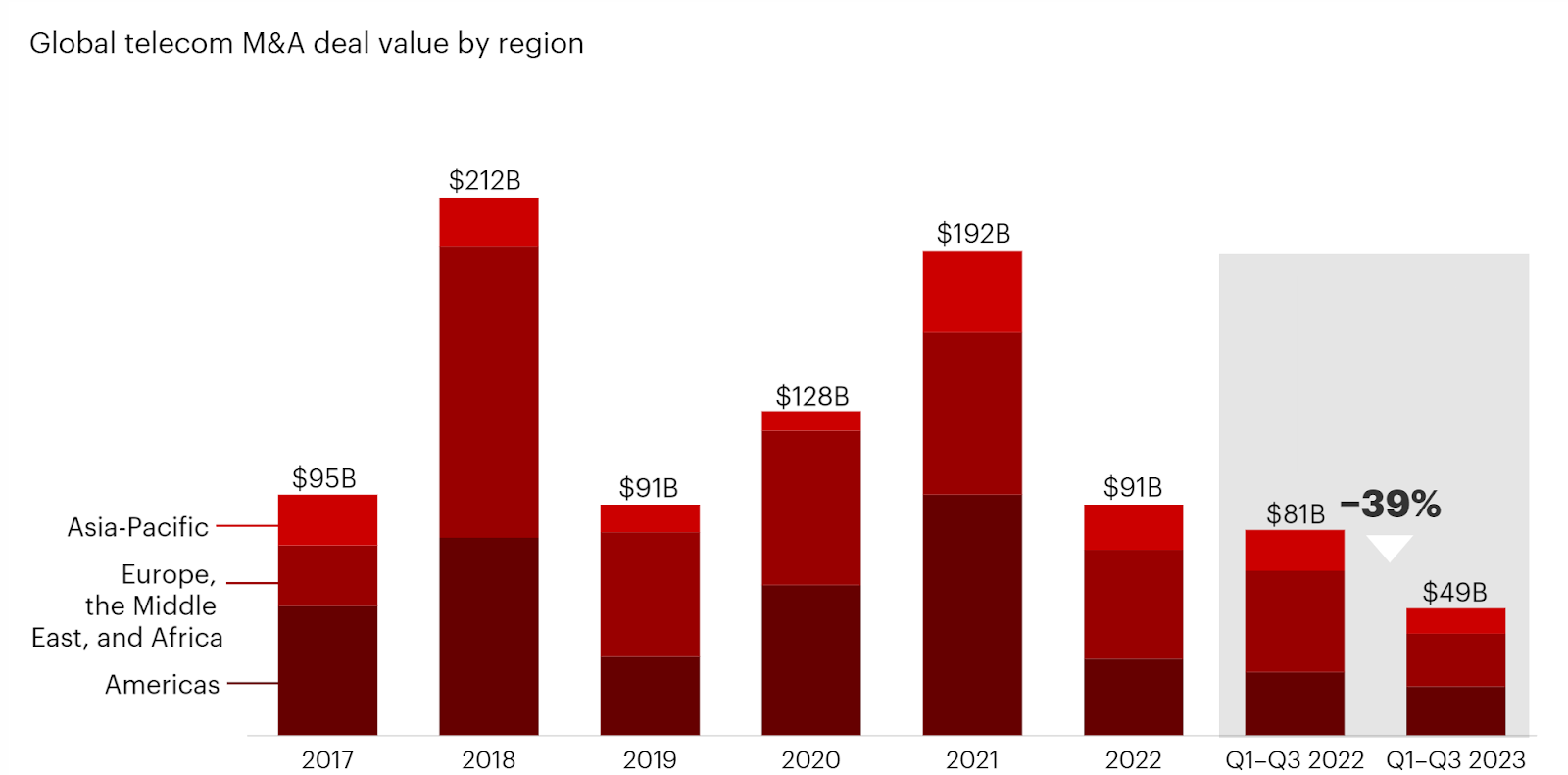

With significant industry transformation and emerging competition, many telcos are turning to M&A to adapt and enhance their capabilities. However, global telecom M&A activity has experienced a notable slowdown, with deal value reaching only $49 billion year-to-date in 2023, according to Bain’s latest report.

This marks a 39% decline from the $81 billion of deal value seen in the same period in 2022, with high-interest rates and capital constraints, compounded by the need for telcos to invest heavily in network upgrades, largely to blame.

However, we would characterize the recent trends as more of a market shift than a decline. The telecom market is seeing less massive platform transactions, bringing the overall deal value down, but transaction volumes are remaining steady.

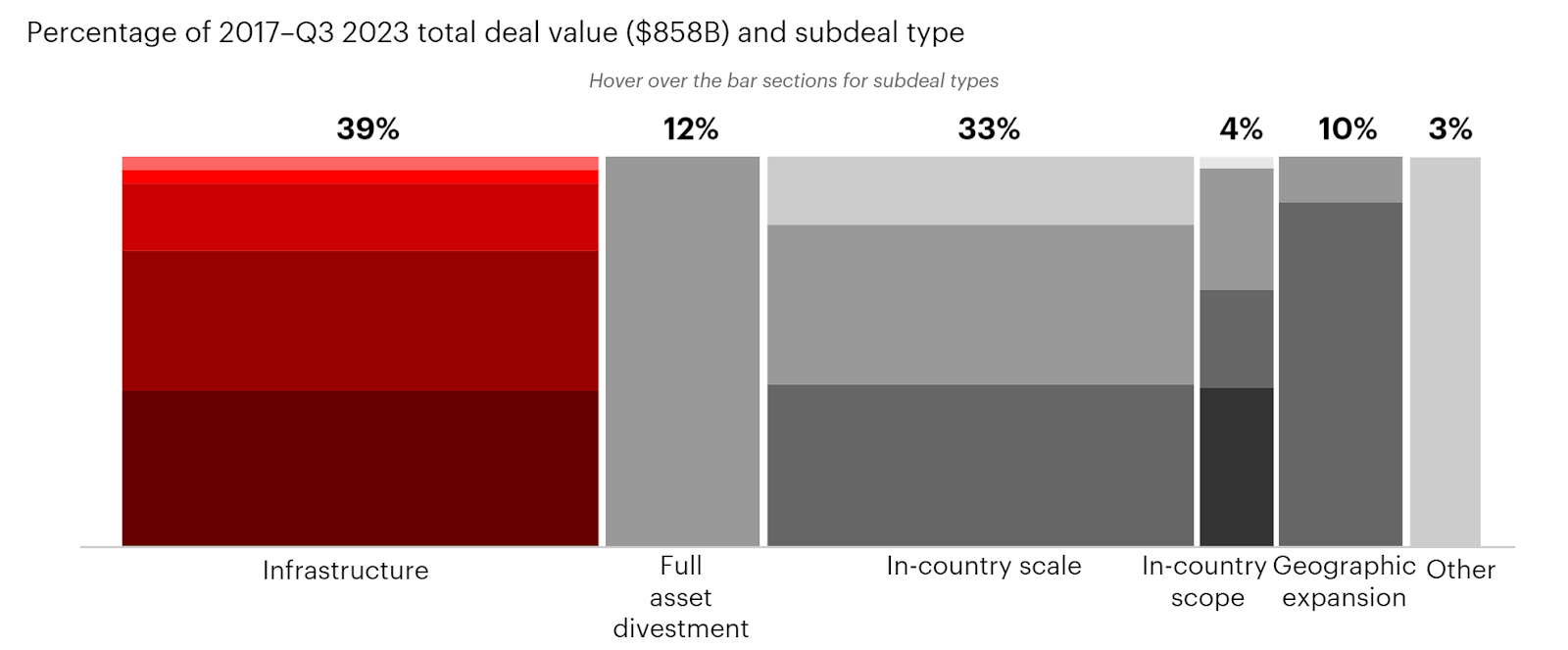

An interesting trend observed is that Q3 saw an infrastructure dominance, where infra deals made up 52% of global deal value, up from its longer-term average of 39%. This is driven by the disaggregation of telecoms, where larger telcos are selling off their heavy-duty assets to free up cash.

This is opening up opportunities for private equity operators to enter the space and dominate verticals. The opportunity in the lower end of the market is even more noticeable, as deal sizes have decreased by roughly half compared to the same period in the previous year.

These trends suggest a shift in the telecom industry toward more focused and disaggregated business models, with infrastructure deals playing a crucial role in realizing this transformation.

Creative Dealmaking to set the Stage in 2024

KKR’s Q3 infrastructure market review also identifies strong opportunities for PEs to acquire from divesting telcos, noting a growing demand for these sorts of transactions in the current macro environment as larger telcos face more pressure on earnings due to sustained inflation and rising interest rates.

In the review, KKR found that most successful transactions in the current environment involved flexibility, access to different pools of capital, strong relationships with companies and management teams, and creativity. PE managers must act creatively not as a way to take more risk, but as a tool to ensure ample downside protection.

One example of this is a sale-leaseback arrangement instead of a spinoff. Companies can unload cost-center assets that would not achieve a high price sold individually and then allow a private operator to own and operate the asset. The PE operator then arranges a team skilled in improving operations and processes and contracts the asset with the original owner.

KKR warns that the challenges of a leaseback involving carving out asset-heavy entities out of larger corporations are significant and that aligning people and culture is often the top concern in a carveout. However, successful sale-leasebacks create outsized value for the PE operator, who is able to acquire a high-quality, de-risked asset, and the corporation, which retains the operating benefits of the asset while improving balance sheet flexibility.

About Us

Panther Equity Group is a private equity firm focused on making investments within the IT & Telecom Services, Technology Services, Business Services & eCommerce verticals.

Our team and Operating Partners have decades of experience within the mentioned verticals along with a vast network of experienced operators and LP investors.

We have the Operational, Technology, M&A, Business Development, and industry-specific Strategy expertise to help companies accelerate their growth and reach their full potential. Learn more about Panther Equity Group by heading over to our website:

A Trusted Partner For Founders, Companies & Entrepreneurs

Industry Commentary

AI & ML

📖 Gartner Worldwide Cloud Public Forecasts

Cloud

📖 Artificial Intelligence & Machine Learning Report

IT Infrastructure

📖 Top Trends Impacting Infrastructure and Operations

M&A

🎤 How antitrust will continue to affect US regulation in our current environment

Broader Market Chatter

2024 Predictions: IT Services Trends

IT services industry trends for 2024 are expected to include familiar themes such as cost optimization, guarded innovation, and genAI. Macro trends such as inflation, interest rates, recession threats, and geopolitical uncertainty are anticipated to continue shaping the industry throughout the coming year.

The top five trends, as outlined by TechTarget, include:

Cloud Cost Optimization: Enterprises prioritized cost optimization in 2023 due to economic challenges, and this focus is expected to persist even stronger in 2024.

Focused Transformation, Innovation: Organizations are expected to allocate more budget and velocity to transformation projects, especially in areas like supply chain transformation and the shift to subscription-based models.

Investment in Generative AI Skills: As organizations prioritize AI in their 2024 innovation budgets, service providers are gearing up for the deployment of generative AI.

Vertical Market Focus: IT service providers will explore opportunities to apply emerging technologies, including AI and data analytics, within specific vertical markets.

Partner Programs, Reconsidered: Technology allies are expected to adjust partner programs in 2024, moving away from tiered structures and towards programs emphasizing co-selling, partner specialization, and differentiation.

Overall, the industry is preparing for continued economic challenges, rapid developments in AI, and a shift towards more focused and transformative initiatives in the coming year.

We’re Looking For Deals 🎯

Our team is focused on making investments within the IT & Telecom Services, Technology Services, Business Services & eCommerce verticals. Along with our operating partners, we have decades of experience within the mentioned verticals paired with a vast network of experienced operators and LP investors.

Size: EBITDA of $2 million – $12 million / $10M to $100M enterprise value

Geography: U.S. or Canada headquarters

Target Transaction: Majority, significant minority, and structured equity investments

Business Profile: Founder or closely-held ownership with an experienced management team

If you’re a Founder / Shareholder interested in working with Panther, or an intermediary with a deal to share — feel free to reach out and get in touch with us! We are happy to compensate fees to intermediaries & referrals at market levels.

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.