Software Remains Unscathed by Q3’s Headwinds

Software Remains Unscathed by Q3’s Headwinds

Panther Equity Insights -- a private equity newsletter covering all things IT & Telecom, Tech & Business Services, eCommerce and Markets.

Happy Wednesday folks! Welcome back to this week's edition of Panther Equity Insights, the bi-weekly newsletter from Panther Equity Group.

In this issue, we’re giving you insights and updates on the industries we specialize in. We’re also covering some broader macro commentary that we believe will be valuable to our network of readers.

Before we begin, if you’re a company Founder / Shareholder interested in working with Panther, a deal maker interested in connecting or with a deal to share, or an Operating Executive looking for a part-time, full-time, or Board Level Role — feel free to reach out and get in touch with us!

Private Market Movements

Credit Fundamentals Present Mixed Bag

In Q3, credit fundamentals appeared robust despite high interest rates and sluggish earnings growth. Debt-to-EBITDA ratios in U.S. leveraged credit decreased to around 4.0x from a peak of 6.5x in 2020. However, Oaktree highlights a significant risk in leveraged loans despite seemingly healthy averages in their latest report, warning of tail risk amongst lower quality borrowers.

As seen above, a noticeable quality gap has emerged between high yield bonds and leveraged loans in the U.S. Nearly 50% of high yield bonds are now rated BB or higher, nearing a 10-year peak, while only about 30% of leveraged loans share this rating.

This divergence is fueled by the surge in leveraged loans for highly leveraged industries, such as technology, and the interest rate sensitivity of loans, leading to increased interest expenses amid slowing EBITDA growth. This could strain overleveraged borrowers, with projections indicating potential struggles in servicing debt over the coming year.

This makes it even more crucial for tech PE operators to focus on cash flow optimization if they want to take advantage of leveraged loans, which typically provide better rates and more leverage compared to bonds. With constrained lending, successful LBOs in the current market will have to face intense scrutiny of interest coverage ratios and other debt metrics.

Implications for PE Portfolio Companies

Traditional buyout PE may continue feeling strains for the next quarter or two, with recent deals seeing senior leverage of only ~3.5x EBITDA and average equity contribution from sponsors growing to ~50-60%. To add to the pain, average yield spreads have widened by 100-150 bps since 2021.

However, since these recent deals are difficult to execute profitability, they have relatively strong credit fundamentals and are at little risk of default.

Instead, risk is concentrated around deals done prior to 2022 when credit requirements were not as stringent. And as a result, GPs should be actively monitoring deteriorating credit scenarios among portfolio companies and preparing scenarios for those with cash flow troubles.

How does Panther think through this? —> Pick creative and nimble Credit partners where possible that have a stomach for volatility, have vested interest in Equity growth and where possible, Equity interests as well. This may not be a fit for all Senior Lenders or Bank Lenders, but there are many of Sub, Junior & Mezz Lenders in the LMM that can form a strong alignment with Sponsors or Companies. If Panther can help you or your Company meet a creative or flexible Credit partner, do not hesitate to reach out!

About Us

Panther Equity Group is a private equity firm focused on making investments within the IT & Telecom Services, Technology Services, Business Services & eCommerce verticals.

Our team and Operating Partners have decades of experience within the mentioned verticals along with a vast network of experienced operators and LP investors.

We have the Operational, Technology, M&A, Business Development, and industry-specific Strategy expertise to help companies accelerate their growth and reach their full potential. Learn more about Panther Equity Group by heading over to our website:

A Trusted Partner For Founders, Companies & Entrepreneurs

Industry Commentary

AI M&A

🎤 Unlocking the AI M&A Supercycle

Venture Capital

📖 Bain Global Venture Capital Outlook

IT

🎤 Guiding the IT Buying Journey

Broader Market Chatter

Software & SaaS Remains Unscathed by Q3’s Macro Headwinds

‘Higher-for-longer’ interest rates and ongoing inflation has caused uncertainty in nearly all industries, but software, SaaS & Digital Transformation businesses continue to show strength as relatively unscathed outliers. Rates have become the focus of all investors and operators as The Fed raised rates from 5.25% to 5.5% in Q3, but held off further rate hikes in its September 20th meeting with the indication of future possible hikes.

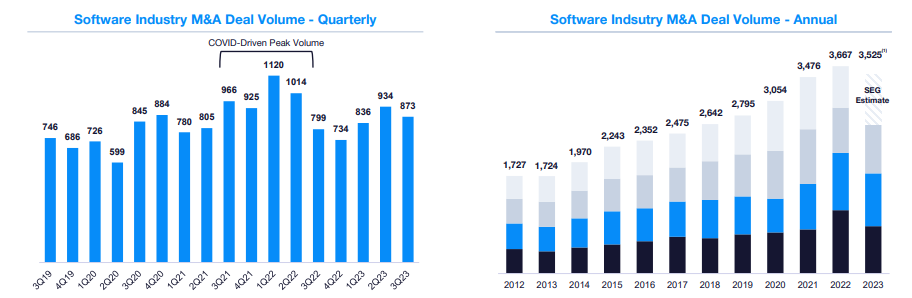

As a result, most industries saw M&A activity collapse in Q3 as deal economics deteriorated. Software marks an exception though, with SEG reporting deal activity increasing 9% YoY this past quarter in their latest research report.

As seen above, the secular digital trends in software are keeping activity significantly above pre-COVID levels. M&A activity is expected to surpass all prior years in 2023, with the exception of the unprecedented boom year of 2022. SEG describes the market as healthy and stable, with continued strength supported by long-term trends of digitalization, AI, IoT, and more.

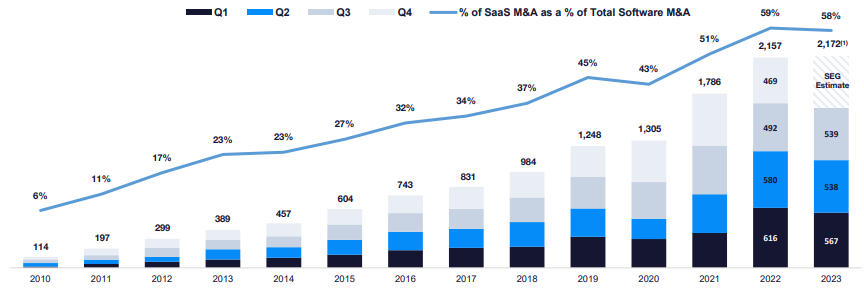

Software deals are surpassing pre-2021 levels, but SaaS is expected to achieve a record year of deal activity in 2023, as seen in the chart above. The uplift in SaaS M&A is proving to be much more than a COVID trend, as global businesses are continuing to adopt cloud-based, modern technology.

For the first time since 2018, the SaaS index EBITDA margin is positive at 1.7% in Q3, a significant gain from -10% in Q3 2022. SaaS companies have rapidly pivoted towards profitability as investors prize cash flow, and they have increased cash margins to 12% this quarter compared to 5% a year ago. Many have found ways to cut back on discretionary S&M and G&A spend, decreasing spend as a % of revenue, while still holding R&D expenses constant to continue product investment for future growth.

SaaS investors should determine whether their portfolio companies have kept up with the strong organic performance of the sector, and determine other areas to optimize costs and efficiency. The current market is rewarding those that demonstrate stable, profitable growth rather than the ‘growth-at-all-cost’ models seen previously.

ERP & Supply Chain Dominate Profitability Indicators

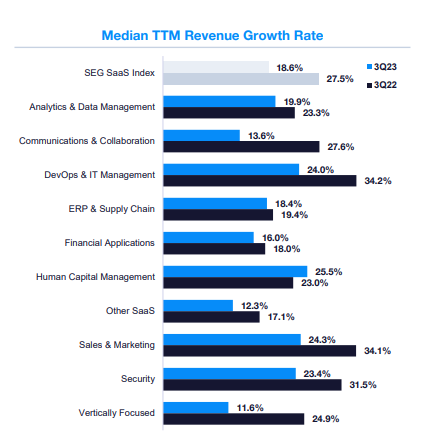

Revenue growth rates have declined across most SaaS categories, understandably so, but ERP & Supply Chain stand out with their ability to maintain 18.4% growth in Q3 2023 compared to 19.4% in Q3 2022. SEG notes this is due to the mission-critical nature of the product category, as many businesses continue to operate through their ERP systems.

Other notable sectors include DevOPs & IT Management, Sales & Marketing, and Security, which all recorded growth rates higher than the industry. Security’s 23.4% growth rate is due to company’s needs to counter increasingly frequent cybersecurity threats, while DevOps & IT

Management’s 24.0% growth is mainly due to the rapid introduction of AI.

In terms of profitability, ERP & Supply also stand out as the most profitable category, achieving 21.2% median EBITDA margins this quarter. The category has achieved a stable, mission-critical status where it can focus on cost optimization and efficiency whereas other categories like DevOps and IT Management remain cash burners.

SaaS investors and operators in negative margin categories should be able to demonstrate concrete plans to profitability and cash flow stability if they wish to receive attractive valuations in today’s market. Today’s environment has much less appetite for risk and places emphasis on cash flow certainty, especially in tech private equity.

We’re Looking For Deals 🎯

Our team is focused on making investments within the IT & Telecom Services, Technology Services, Business Services & eCommerce verticals. Along with our operating partners, we have decades of experience within the mentioned verticals paired with a vast network of experienced operators and LP investors.

Size: EBITDA of $2 million – $12 million / $10M to $100M enterprise value

Geography: U.S. or Canada headquarters

Target Transaction: Majority, significant minority, and structured equity investments

Business Profile: Founder or closely-held ownership with an experienced management team

If you’re a Founder / Shareholder interested in working with Panther, or an intermediary with a deal to share — feel free to reach out and get in touch with us! We are happy to compensate fees to intermediaries & referrals at market levels.

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.