SaaS M&A Remains Elevated

Panther Equity Insights -- a private equity newsletter covering all things IT, Tech, Business Services, eCommerce and Markets.

Happy Thursday, folks! Welcome back to this week's edition of Panther Equity Insights, the bi-weekly newsletter from Panther Equity Group.

This week we’re looking at:

State of SaaS M&A in 2024

Industry Commentary on Digital Transformation, SaaS, and AI

Private market insights on the Latest US Macro Data

Our aim is to provide you with the latest insights and advancements in these verticals, along with valuable perspectives. We strive to create a newsletter that is informative and thought-provoking for all market participants.

We’re Looking For Deals 🎯

Our team is focused on making investments within the IT Services, Technology Services, Business Services & eCommerce verticals. Along with our operating partners, we have decades of experience paired with a vast network of experienced executives and LP investors.

Size: EBITDA of $2 million – $12 million

Geography: U.S. or Canada headquarters

Target Transaction: Majority, significant minority, and structured equity investments

Business Profile: Founder or closely-held ownership with an experienced management team

Additionally, Panther is actively looking for ‘add-on’ investments that meet the following criteria:

Industry: IT Digital Transformation / Software Dev 💻

Size: Up to $4 million in EBITDA

Geography: Flexible

Target Transaction: Majority recapitalization

If you’re a Founder / Shareholder interested in working with Panther, or an intermediary with a deal to share — feel free to reach out and get in touch with us! We are happy to compensate fees to intermediaries & referrals at market levels.

Broader Market Chatter

SaaS M&A Remains Elevated

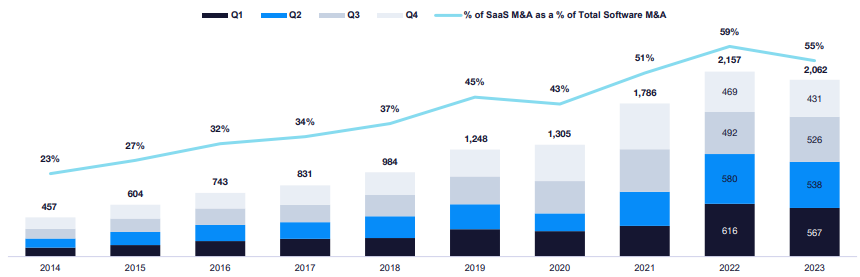

The overall volume of deals in the software industry has stabilized at an elevated level compared to historical norms. According to SEG’s recent 2024 SaaS report, 2023 saw a total of 3,333 deals, marking a 9% increase over the figures from 2020. This demonstrates a consistent upward trajectory when compared to the pre-COVID era, with 2021 and 2022 standing out as exceptionally active years.

The data for SaaS M&A differs vastly though, as the sector has far outperformed its pre-COVID levels. SaaS M&A in 2023 reached the second-highest number of transactions on record, following closely behind the figures from 2022.

Despite the overall software M&A returning to pre-COVID trends, the volume of SaaS M&A transactions stands significantly higher, showing increases of 15% and 58% compared to 2021 and 2020, respectively. In 2023, SaaS saw 2,062 deals, as seen above, and accounted for 55% of all aggregate software transactions, marking the third consecutive year SaaS represented more than half of total software deals.

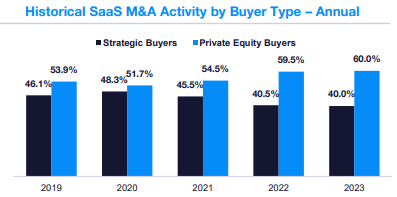

SaaS M&A is Dominated by Middle Market PE Investors

The latest SaaS M&A data shows a notable increase in the number of low-multiple, middle-market deals, which lowered median transaction multiples. The heightened volume of lower sized deals can be attributed to various catalysts such as dwindling cash reserves, challenging debt dynamics, competitive pressures, or investors choosing to divest their underperforming assets to focus on stronger performers.

While valuations seem to be at the low-end compared to recent years, SaaS operators believe the impending rate cuts will bring SaaS towards a higher valuation environment.

Due to the attractive valuations, PE investors have come in to dominate the M&A market, with PE comprising 60% of acquirers in 2023. This is strengthened by the fact that public SaaS strategics have seen poor share performance, reducing their ability to compete in acquisitions.

However, if the trends in Q4 are indicative of the future, the momentum might be shifting back in the opposite direction. Strategic buyers, accounting for 44% of Q4 SaaS deals, experienced their most active quarter since 1Q22.

Private equity is anticipated to remain influential in 2024, but the resurgence of public company buyers leads many to anticipate increased strategic acquisitions. Overall, SaaS is well positioned for a strong M&A year in 2024, with macro conditions improving, digital trends retaining momentum, and both strategic and PE acquirers strengthening their financial position.

About Us

Panther Equity Group is a private equity firm focused on making investments within the IT Services, Technology Services, Business Services & eCommerce verticals.

Our team and Operating Partners have decades of experience within our focus verticals along with a vast network of experienced operators and LP investors.

We have the Operational, Technology, M&A, Business Development, and industry-specific Strategy expertise to help companies accelerate their growth and reach their full potential. Learn more about Panther Equity Group by heading over to our website:

A Trusted Partner For Founders, Companies & Entrepreneurs

Industry Commentary

AI

📖 AI optimism is powering industrials stocks, too

Digital Transformation

📖 Technology in Retail: Escaping the Complexity Trap

SaaS

🎤 The SaaS Revolution Show

If you’re a company Founder / Shareholder interested in working with Panther, a deal maker interested in connecting or with a deal to share, or an Operating Executive looking for a part-time, full-time, or a Board Level Role — feel free to get in touch with us!

Private Market Movements

Macro Tailwinds Strengthen as The Fed Reveals Bullish Forecasts

Macroeconomic conditions are finally normalizing based on findings in KKR’s latest macro update, and investors and operators alike stand to benefit.

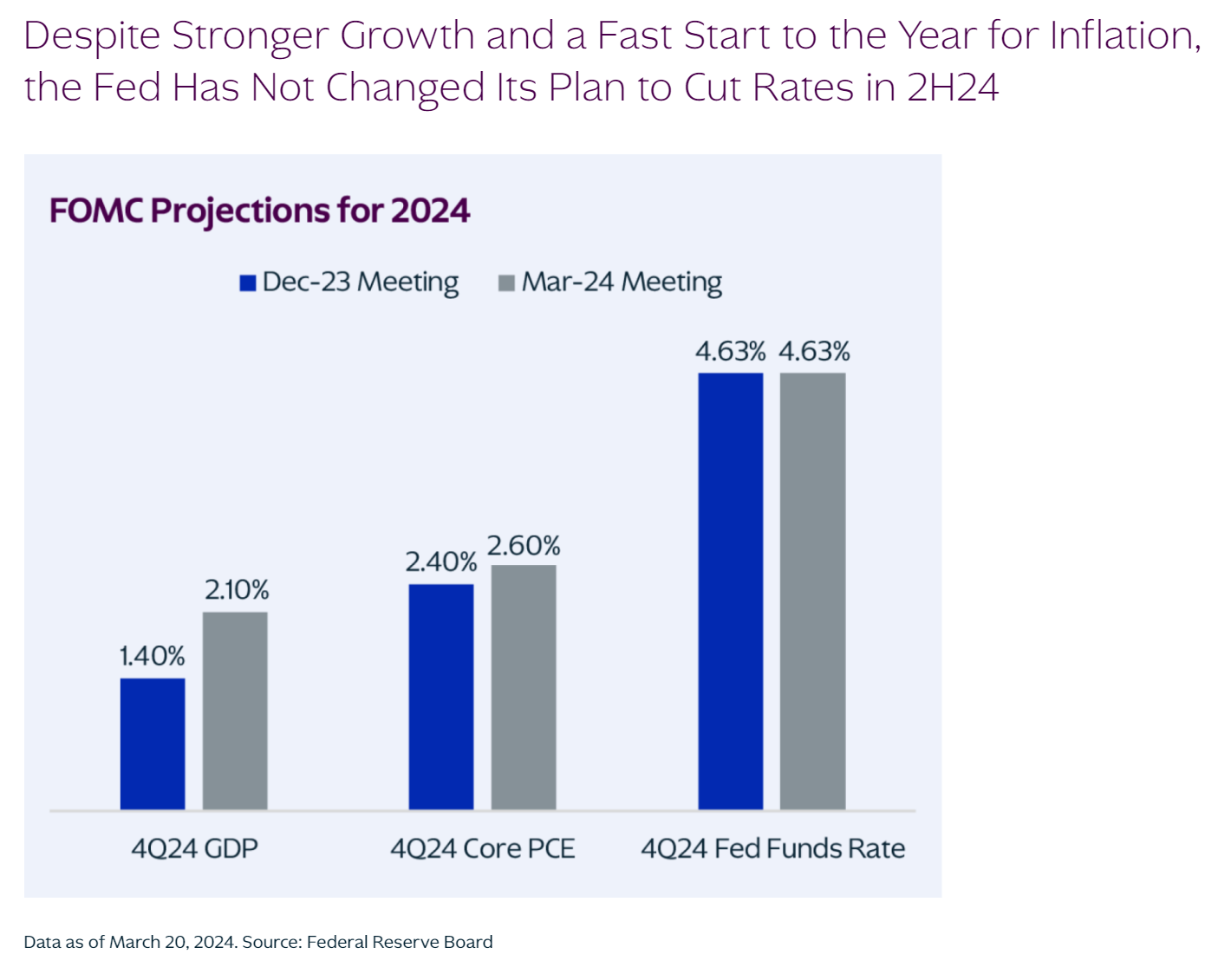

The Federal Reserve forecasts both stronger economic growth and inflation, indicating that the economy is coming into better balance. FOMC members have upgraded GDP forecasts significantly from 1.4% to 2.1% in 4Q 2024, attributing it to increased labor supply and cooler rent growth.

Fed Chair Jerome Powell maintains that rate cuts will likely be appropriate in the latter half of 2024, most likely in June, to hold real rates to around two percent. The Fed plans for three rate cuts this year, but analysts at KKR expect only two due to the longer duration of inflationary pressures.

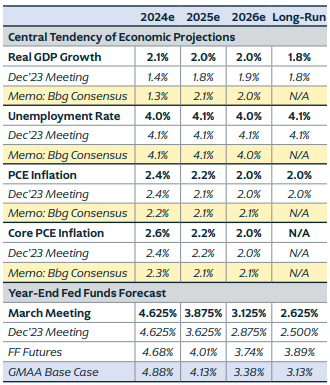

KKR maintains a bullish outlook on interest rates, growth, and inflation and expects resilient GDP growth and moderating but still elevated inflation moving forward. They predict the Fed may struggle to fully restore inflation to its two-percent target, leading to expectations of rates settling at 3.125% over the longer term compared to the Fed's expectation of 2.625%, as seen below.

Overall, KKR’s analysis highlights long-term forecasts indicating robust GDP growth, stable unemployment and inflation, and a normalization of interest rates. Federal Reserve policy also points towards strengthening market and macroeconomic conditions, but how does this translate into investment decisions? Let's delve into some main themes:

"Coming into better balance": The Fed's latest report suggests a more balanced economy and favorable market environment, with a projected upward revision in 4Q24 GDP growth of approximately three percent. However, uncertainties remain regarding the depth of rate cuts due to the balanced labor market and declining inflation. PE investors can anticipate improving, though not excessively bullish, economic conditions in the near future.

"Higher for Longer" Inflation and Unchanged Interest Rates: The Fed has raised its 2024 Core PCE inflation forecast to 2.6%, acknowledging a world where inflation frequently surpasses its two percent target. Upward revisions in the forecasts for 2025 and 2026 imply a longer-term adjustment to heightened inflation expectations. Portfolio companies with inflation protection attributes are expected to remain in high demand over the coming years.

What to Monitor: It's crucial to keep a close eye on deviations from projections, particularly in the event of unexpected collapses in inflation or surges in unemployment.

Investment implications suggest a market-friendly environment with anticipated Fed rate cuts expected to bolster momentum. KKR holds a bullish stance on contracted assets that have favorable tailwinds and built-in inflation protection.

In the case of SaaS, this would mean negotiating contracts that have robust escalation clauses as they will be valued highly by investors and acquirers. Overall, all investors will benefit from a strengthening macro backdrop and this tailwind will help SaaS and the overall software industry retain elevated levels of M&A and investment.

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.