Private Lenders Move on SVB Crash

Private Lenders Move on SVB Crash

Panther Equity Insights -- a private equity newsletter covering all things IT & Telecom, Tech & Business Services, eCommerce and Markets.

Welcome back to another edition of Panther Equity Insights! If you're new here, we're thrilled to have you on board. Every other week, we offer industry insights and thought leadership on IT & Telecom Services, Tech & Business Services, and eCommerce.

In this week's edition, we'll cover:

2023 Digital Commerce M&A Outlook

Private Lenders Move on SVB Crash

IT Services Sector Priorities for 2023

Don't forget to subscribe to stay up to date with our latest insights. If you find the content valuable, feel free to share it with your network!

Before we begin, here’s a quick intro to Panther Equity Group:

About Us

Panther Equity Group is a private equity firm focused on making investments within the IT & Telecom Services, Technology Services, Business Services & eCommerce verticals.

Our team and Operating Partners have decades of experience within the mentioned verticals along with a vast network of experienced operators and LP investors.

We have the Operational, Technology, M&A, Business Development, and industry-specific Strategy expertise to help companies accelerate their growth and reach their full potential.

Whether you’re a company Founder / Shareholder interested in working with Panther, a fellow deal maker interested in connecting, or an intermediary with a deal to share (we are happy to compensate for introductions & referrals) — feel free to reach out and get in touch with us!

Broader Market Chatter

IT Services Sector Priorities for 2023

While the last few years of technological disruption have resulted in unprecedented growth for the cybersecurity sector, it has also created a heightened risk of cyber-attacks, breaches, and bad actors taking advantage of emerging trends like teleworking and remote work.

Security vendors, VARs and MSPs are working to stay ahead of these threats and are collaborating with their channel partners to provide new security solutions to customers. A study from CRN polled the CEOs of the worlds leading cybersecurity companies on their priorities. Some noteworthy answers:

Empower channel partners through solutions that are tailored to how customers want to consume their services

Unlocking growth with resellers and service providers

Diversification by customers, geography, and industry to fuel growth

Adapting solutions proactively to defend against the constantly evolving cyber threats

Simplifying product offerings and platform solutions

Evolving integrations with technology partners to support expansion

It seems that there are a few key underlying themes that surround these initiatives, which include supporting channel partners, improving offerings, and optimizing go-to-market initiatives.

Our outlook on these initiatives:

The ‘paranoid’ and foreword thinking Service providers in Technology & IT will thrive while those that are comfortable and staying still will (i) risk customer loss, (ii) difficulty to increase existing wallet-share with customers and (iii) challenges with retaining top-talent / recruiting new members. In parts of IT & Security today, companies need to run to just stay in place. Panther + our Operating Partner bench love talking about all things ‘IT, Tech & Digital Transformation’ — please feel free to reach out if we can ever be helpful.

Industry Commentary

Cyber Security

Deal Alert: Rapid7 is set to acquire Minerva Labs for $38M

Boston-based security vendor, Rapid7 announced earlier this week that it acquiring Minerva Labs, an anti-evasion and ransomware prevention technology provider. It was stated that the acquisition will help Rapid7 extend its managed threat detection offering with capabilities for the orchestration of “advanced” ransomware prevention.

IT Services M&A

Despite the slowdown in 2022, digital transformation remains a high priority for most organizations. Besides stable demand, IT Services also tend to operate with robust fundamentals, including relatively stable revenue growth and margins and asset-light operations. Therefore, we expect continued interest from strategic and financial investors and the M&A activity to resume its upward trend as market conditions improve.

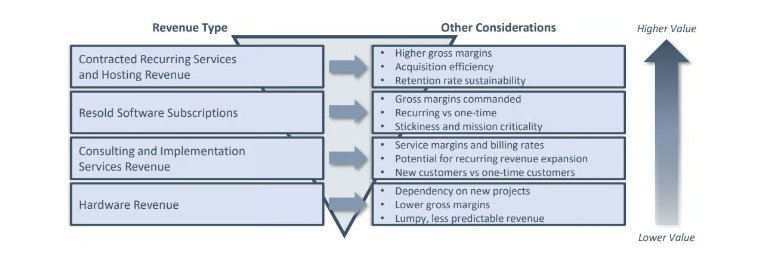

MSPs

What’s covered in this breakdown:

MSP Service Landscape

Characteristics Drive Value & Opportunity

Revenue Type Impacts Valuation

E-commerce

Private Market Movements

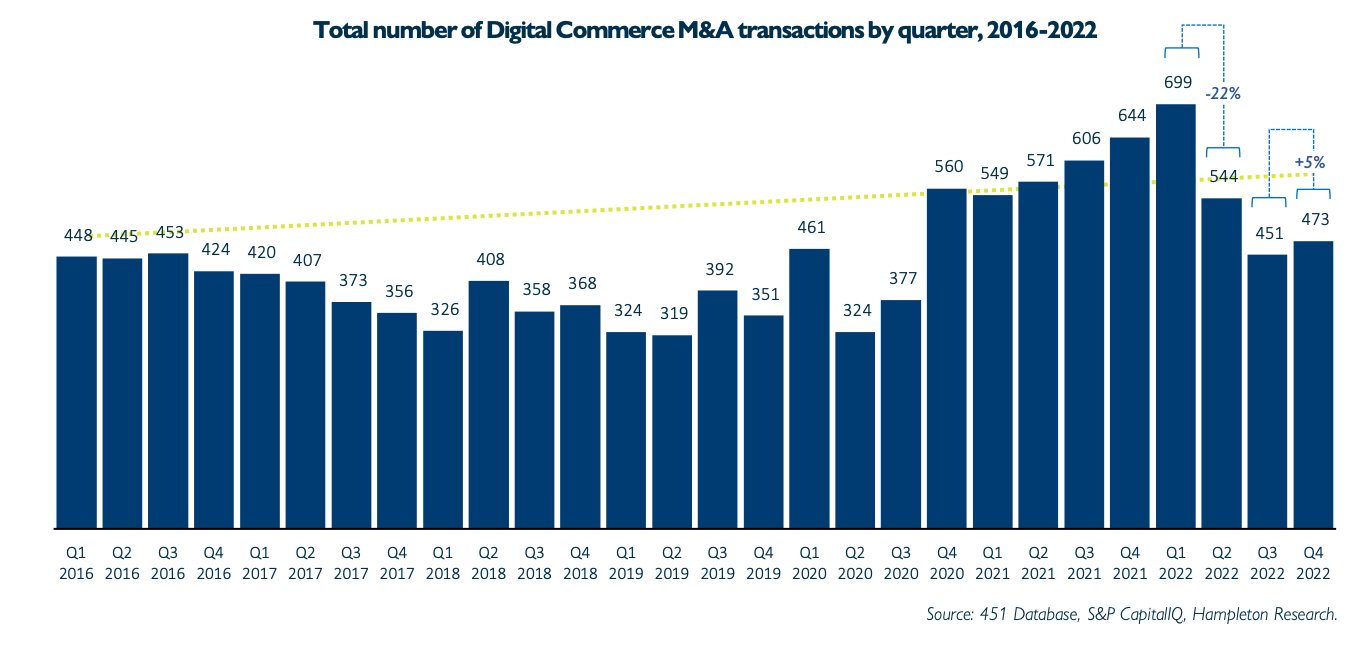

2023 eCommerce M&A: Back to a new normal

The eCommerce M&A market has landed from a pandemic-induced high. Although this may be a sign of concern given the current macro outlook, M&A professionals believe it’s a sign of a stabilizing maturing market. Since pandemic highs in 2021, the global online retail index share price has dropped by 51%. That being said the deal activity in the private sector has only dropped by 9%.

M&A in eCommerce public markets are currently not the right proxy for private deal data and not directly comparable for the market’s transaction volume. Contrary to public comps, Panther sees the eCommerce market as relatively mature and stable within the global economy in certain end-product focuses.

A recent report from Hampleton Partners outlined the 2023 outlook for eCommerce M&A. Some notable figures include:

In 2022 the industry saw a total of 2,167 deals, which is only a 9% decrease from the record figures of 2021. Compared to other industries, which experienced 20%+ drops in M&A volume, this slight pullback is a sign of healthy stabilization.

Active acquirers decreased from 14% to 7% in the second half of 2022. The report noted that the backward trend is a result of acquirers being hesitant to deploy capital despite holding on to record amounts of dry powder.

Private Lenders Set to Capitalize on SVB & Recent Bank Fallouts

After the recent fall of SVB, non-bank lenders (i.e., private credit, SBICs) are seeking to increase their market share and capitalize on the gap in the private debt market. While SVB has resumed its deposit and lending services, private lenders are experiencing a surge in demand from both venture-backed companies & PE targetCos in need of credit.

Other banks that have since been seized by regulators or ‘fire-sold’ to competitors at discounts include:

New York-based Signature Bank, which regulators seized last week, will be acquired by a unit of New York Community Bancorp. The subsidiary, Flagstar Bank, is assuming customer deposits and some loan portfolios

Switzerland's UBS agreed to buy Credit Suisse for 3 billion Swiss francs ($3.2 billion) in stock, in a hastily arranged deal on Sunday. The Swiss government and central bank backed the transaction by providing liquidity in addition to protecting UBS from potential losses. The combined entity will oversee $5 trillion in invested assets.

Although Panther & many PE firms in the ‘lower mid-market’ (i.e., $10M to $100M transaction focus) may not interact regularly with these banks — this speaks to the broader themes of uncertainty, risk and investors & Sellers being creative in order to have deals materialize.

Chart of the Week

According to Bain Private Equity's recent report for 2023, investments made coming out of a downturn typically generate superior returns over time. The reasons behind this trend are twofold:

Top firms continue to identify and pursue investment opportunities that align with their investment thesis and are thoroughly vetted against macroeconomic factors.

Firms remain assertive and undeterred by adverse market conditions. Waiting for optimal conditions risks losing out on valuable opportunities to profit from the eventual rebound.

Panther Equity Insights <> Deal Bridge Media

This newsletter was powered by the team at Deal Bridge Media. Deal Bridge builds newsletters for M&A firms to help them generate more inbound deal flow.

Does your investment firm want to start a newsletter? Get in touch with Deal Bridge today!

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.