Outlook on the Software Market in 2024

Outlook on the Software Market in 2024

Panther Equity Insights -- a private equity newsletter covering all things IT, Tech, Business Services, eCommerce and Markets.

Happy Wednesday folks! Welcome back to this week's edition of Panther Equity Insights, the bi-weekly newsletter from Panther Equity Group.

This week we’re looking at:

Outlook on the Software Market in 2024

Industry Commentary on E-Commerce, NetOps, Telecom, Digital

Private market insights on the Latest Middle Market PE Data

Our aim is to provide you with the latest insights and advancements in these verticals, along with valuable perspectives. We strive to create a newsletter that is informative and thought-provoking for all market participants.

We’re Looking For Deals 🎯

Our team is focused on making investments within the IT Services, Technology Services, Business Services & eCommerce verticals. Along with our operating partners, we have decades of experience paired with a vast network of experienced executives and LP investors.

Size: EBITDA of $2 million – $12 million

Geography: U.S. or Canada headquarters

Target Transaction: Majority, significant minority, and structured equity investments

Business Profile: Founder or closely-held ownership with an experienced management team

Additionally, Panther is actively looking for ‘add-on’ investments that meet the following criteria:

Industry: IT Digital Transformation / Software Dev 💻

Size: Up to $4 million in EBITDA

Geography: Flexible

Target Transaction: Majority recapitalization

If you’re a Founder / Shareholder interested in working with Panther, or an intermediary with a deal to share — feel free to reach out and get in touch with us! We are happy to compensate fees to intermediaries & referrals at market levels.

Broader Market Chatter

Software Investment Expected to Pickup in 2024

Recently, the software investment landscape has fluctuated due to a volatile macroenvironment. After the period of intense investment in 2021/2022, the sector faced challenges that came with sharp rate-hikes. However, navigating this made software operators more ‘profit oriented’ vs ‘revenue at all costs’…which makes most investors view this upcoming year with optimism.

There's currently a substantial volume of capital available, and CIOs & CTOs are increasing spending again after drastically cutting budgets last year. Additionally, valuations are normalizing and investor interest in software transactions are picking up.

Today, we’ll dive into McKinsey’s latest research on the state of the software market and the key trends expected to shape 2024.

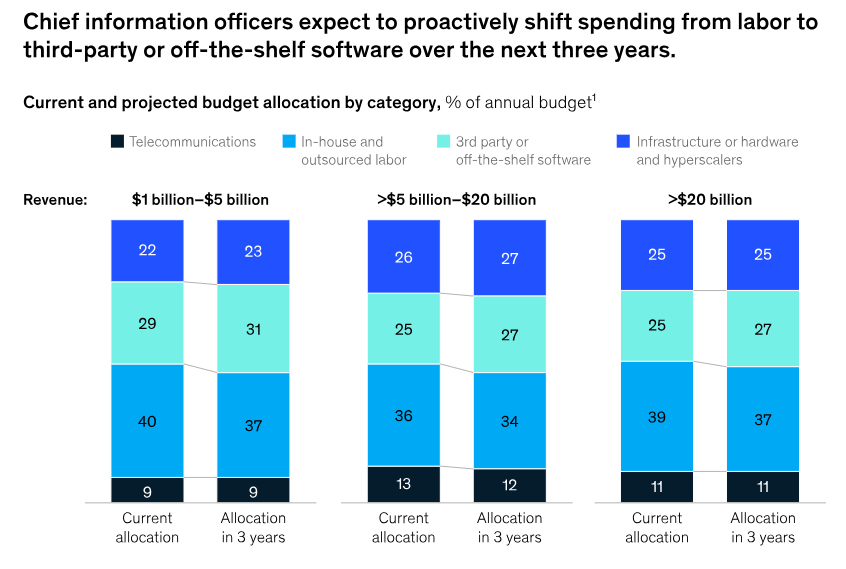

Software Buyers Expect to Increase Spending

In general, CIOs are projected to continue spending on software, driven by a growing reliance on software to enhance operational efficiency as seen in the chart above. 3rd party software is expected to grow and the trend of vendor consolidation will continue, except in areas marked by significant innovation, such as data.

Expenditure is expected to vary across different software categories though. McKinsey's 2023 CIO Survey indicates that spending on cybersecurity and data analytics will rise significantly as companies focus on advancing their generative AI capabilities while safeguarding their application and infrastructure setups.

Generative AI is also forecasted to stimulate expenditure in specific areas where its applications bring incremental benefits, such as sales, supply chain management, customer service, and industry-specific applications. Conversely, spending on human capital management and finance is anticipated to remain relatively stagnant. Software providers should understand how they’re segment will grow and advance over the next few years and develop agile strategies that tap into market growth.

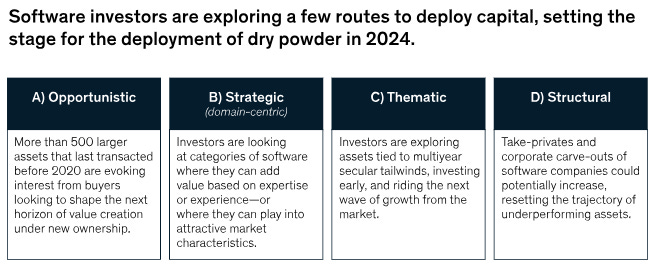

Shifting Software Investment Themes

Investment in the sector is changing. A sluggish 2023 resulted in delayed capital deployment, prompting quicker sales processes for investments held for extended periods. Market uncertainty continues to slow acquisition activity, but opportunities exist for investors to acquire during a downmarket.

Ongoing fragmentation within specific domains, such as data, is expected to open up opportunities for thematic investments. Additionally, investors are increasingly considering long-term strategies, including carve-outs and take-privates.

Recent data also finds that the market highly values operational improvements.

As seen above, a significant gap exists between top-performing and average software companies in terms of value creation, with valuation differences mostly attributed to focused efforts on revenue enhancement and operational efficiency.

Software operators and investors considering a sale within the next 12 to 36 months may benefit from proactively undertaking improvement initiatives. Overall, McKinsey predicts a new wave of software investment over the near term, and now is the time to take investment action rather than remain a passive market participant.

About Us

Panther Equity Group is a private equity firm focused on making investments within the IT Services, Technology Services, Business Services & eCommerce verticals.

Our team and Operating Partners have decades of experience within our focus verticals along with a vast network of experienced operators and LP investors.

We have the Operational, Technology, M&A, Business Development, and industry-specific Strategy expertise to help companies accelerate their growth and reach their full potential. Learn more about Panther Equity Group by heading over to our website:

A Trusted Partner For Founders, Companies & Entrepreneurs

Industry Commentary

M&A

📖 The Top 50 Lower Middle Market Technology Investors & M&A Advisors

We appreciate the recognition by Axial for highlighting Panther Equity Group as an active investor & partner in the Technology Services space

E-commerce

📖 Marketplaces grow faster than other B2B digital sales channels

Digital Trends

🎤 Where AI Is Advancing

If you’re a company Founder / Shareholder interested in working with Panther, a deal maker interested in connecting or with a deal to share, or an Operating Executive looking for a part-time, full-time, or a Board Level Role — feel free to get in touch with us!

Private Market Movements

Middle Market PE Continues Gaining Momentum

The success of US middle-market private equity continues to gain momentum, as highlighted in Pitchbook's recent report. Both buy-side and sell-side activities showed significant growth in deal value and count in the latest data, and the middle market outperformed larger sized strategies for yet another quarter.

This uptick in activity can be attributed to several factors favoring the middle market, including robust fundraising, superior returns, and efficient capital distribution to investors. Additionally, part of this growth stemmed from the influx of rescue capital, restructurings, and distressed asset transactions.

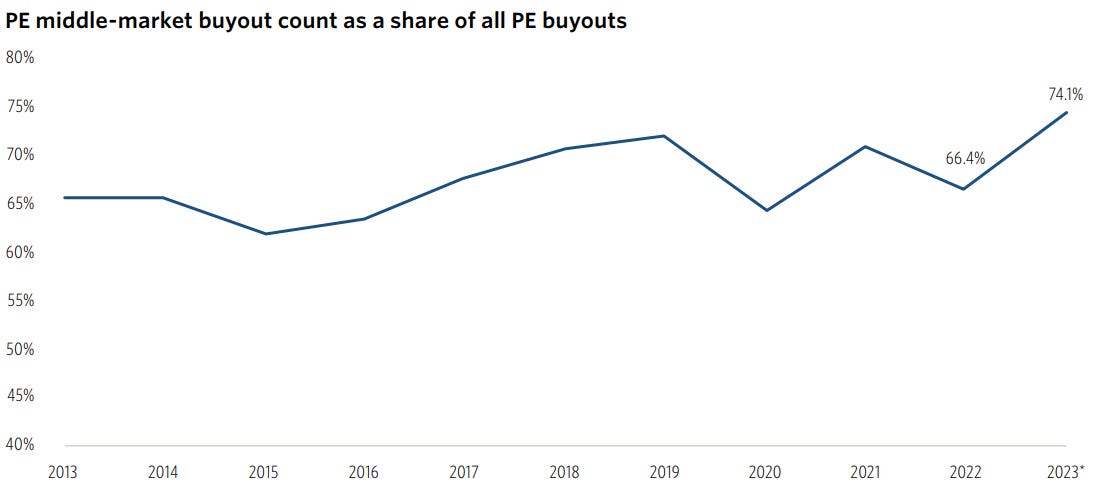

Middle-market PE has consistently been setting new records for its share of total PE buyouts, and Q4 2023 was no exception. As seen above, the middle market now constitutes 74.1% of all deal count, surpassing the 66.4% figure recorded in 2022. Additionally, deal count rose by 4% from 3,549 in 2022 to 3,689 in 2023.

This increase in activity is largely due to the relative outperformance of the middle market compared to mega-funds, as smaller transactions are more viable during periods of high rates. Despite a difficult environment in 2023, the middle market only experienced a decline of 18.9% in buyout value last year compared to the broader PE market's 32.7% decline.

Although the market is performing well given the circumstances, a full recovery hasn't materialized yet, as seen with the deal value decline. Investors will likely need to wait until macro conditions further normalize though LPs can anticipate stable, moderate returns with opportunities for significant performance in the years ahead.

Compared to larger sized strategies, middle-market PE has outperformed mega-funds for most of 2022 and 2023, though returns are now equalizing as the public market rally benefits larger investors more. However, middle-market funds have also benefited from this rally, with valuation growth extending to small and mid-cap companies.

Cash flow is where the middle market leads the competition by far. Recent data from 2023 shows that mid-market managers received $66.3 billion in contributions and distributed $88.7 billion, resulting in a positive inflow of $22.4 billion to investors. In contrast, mega-funds experienced contributions nearly doubling their distributions, leading to a net outflow of -$30.0 billion.

The trend of stronger cash flow in the mid-market is expected to continue, bolstering mid-market managers' position in upcoming fundraising cycles as they consistently return capital to LPs, even amid challenging exit conditions. 2023 marked the mid-market’s strongest fundraising year since 2019, and momentum appears to be growing in 2024.

Investors should consider the benefits of Total Value to Paid-in-Capital (TVPI), even if IRR remains constant. TVPI provides a more realistic representation of returns guaranteed to investors, whereas IRR may factor in theoretical asset values. IRR is also essential though as it captures the time component of returns.

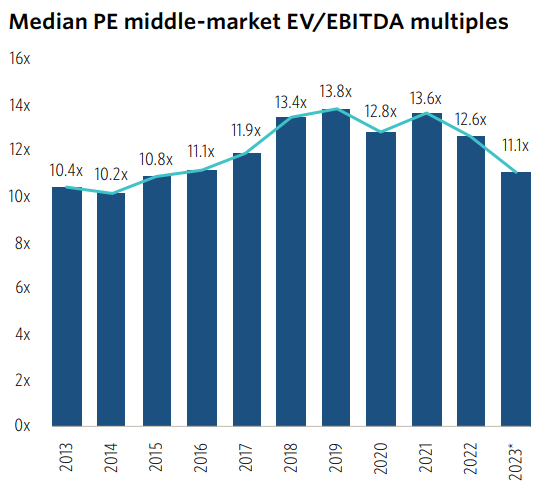

While much of the growth observed in mid-market PE last quarter was driven by positive trends, some of it also stemmed from the expansion of rescue capital and distressed transactions. Decreasing valuations in terms of EV/EBITDA and EV/revenue have created opportunities for PE firms to acquire assets at discounted prices.

This was evident in numerous restructurings during the recent quarter, where underperforming or near-bankrupt companies were acquired with a turnaround strategy. Though this activity is expected to diminish as economic conditions recover, it helps stabilize valuations and presents opportunities for investors.

Looking ahead, the industry's overall participation in a complete recovery relies on an increase in exit activity, which still remains subdued due to market challenges. Investors anticipate that this will be addressed by forecasted rate cuts and a strengthening public market, although uncertainties will persist in the near term. Investors confident in their strategy should capitalize on current lower valuations today to drive greater returns once conditions normalize.

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.