2024 Expectations Within IT & Business Services Remain Positive

2024 Expectations Within IT & Business Services Remain Positive

Panther Equity Insights -- a private equity newsletter covering all things IT, Tech, Business Services, eCommerce and Markets.

Happy Wednesday folks! Welcome back to this week's edition of Panther Equity Insights, the bi-weekly newsletter from Panther Equity Group.

This week we’re looking at:

Industry Commentary on digital supply chain, e-commerce, and cloud M&A

Trends and forecasts in business services and services verticals

Private market insights on KKR’s analysis of private investment structural shifts

Our aim is to provide you with the latest insights and advancements in these verticals, along with valuable perspectives. We strive to create a newsletter that is informative and thought-provoking for all market participants.

We’re Looking For Deals 🎯

Our team is focused on making investments within the IT Services, Technology Services, Business Services & eCommerce verticals. Along with our operating partners, we have decades of experience paired with a vast network of experienced executives and LP investors.

Size: EBITDA of $2 million – $12 million

Geography: U.S. or Canada headquarters

Target Transaction: Majority, significant minority, and structured equity investments

Business Profile: Founder or closely-held ownership with an experienced management team

Additionally, Panther is actively looking for ‘add-on’ investments that meet the following criteria:

Industry: IT Digital Transformation / Software Dev 💻

Size: Up to $4 million in EBITDA

Geography: Flexible

Target Transaction: Majority recapitalization

If you’re a Founder / Shareholder interested in working with Panther, or an intermediary with a deal to share — feel free to reach out and get in touch with us! We are happy to compensate fees to intermediaries & referrals at market levels.

Broader Market Chatter

Business Services & IT Spending Rationalization in Q4, with Rebound Expected

In the fourth quarter, global spending on IT and business services experienced a slight decline, reaching $23.4 billion, down 3% from the previous year, according to a report from Information Services Group (ISG). However, despite this being a consecutive quarter of market decline, the slowdown is flattening, and analysts point to catalysts that could drive a market rebound in 2024.

Before we dive into the numbers, it’s important to define that managed services are a much more comprehensive service offering where the provider takes care of IT management whereas the broader services sector relies on customers’ in-house teams to manage integration. As a result, managed services tend to be far more expensive.

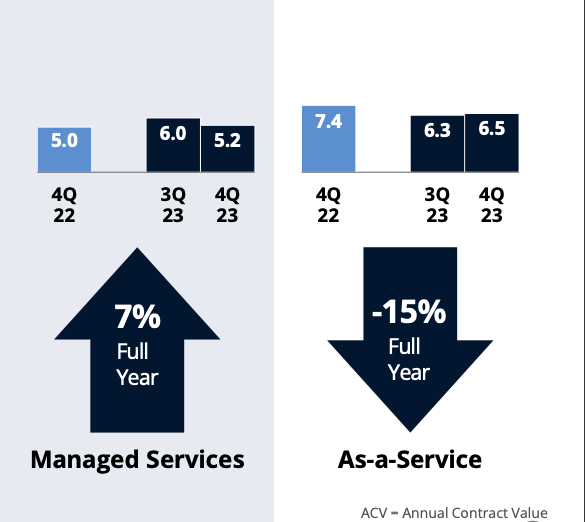

In the North American market, there was a distinct contrast in performance between managed services and the overall As-a-Service (XaaS) market in Q4.

Managed services ACV in Q4 was $5.2 billion, down 13% compared to Q3 but up 7% from the previous year, with several recent large deals in the market providing optimism for further growth. On the other hand, XaaS spending grew a marginal 3% quarter-over-quarter but dropped 15% over the full year to $6.5 billion.

Difficult macro conditions negatively impacted the diverse XaaS market, as customer cost optimization efforts drove down revenue. However, analysts believe the market has moved past the peak of cost optimizations and that pricing and volume should improve this year.

In addition, some XaaS segments, such as infrastructure-as-a-service (IaaS), are showing promising performance gains and are predicted to be only one quarter away from emerging from the downturn and achieving a new phase of growth.

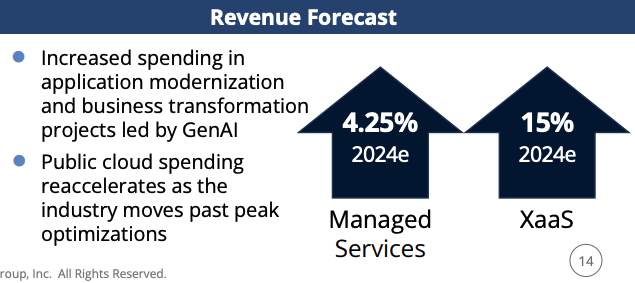

Looking forward, the forecast for 2024 includes 4.25% growth for managed services and 15% revenue growth for XaaS. ISG highlights that AI-related spending on application modernization and business transformation projects, as well as increased public cloud spending, will be two of the most significant tailwinds to watch out for.

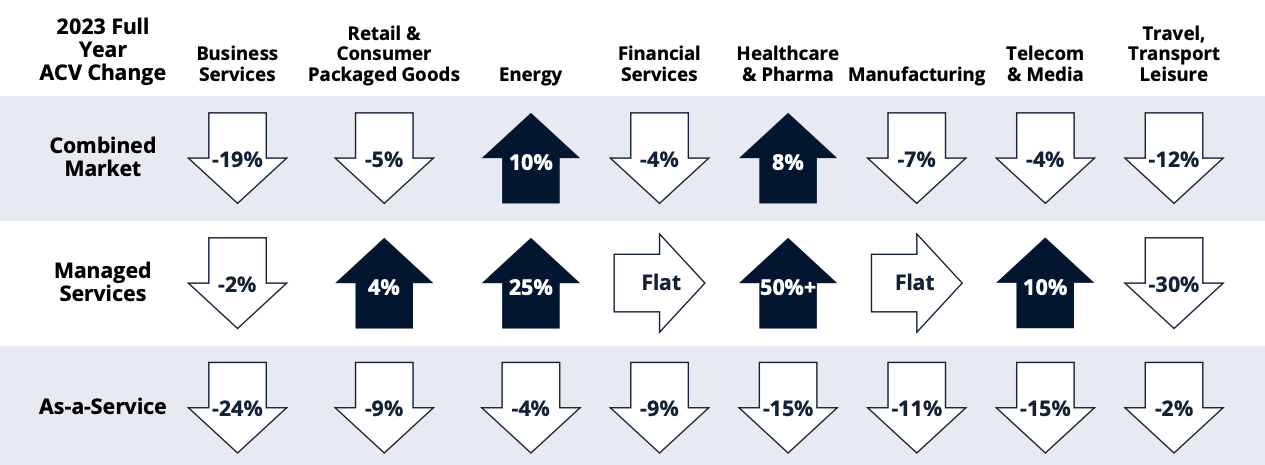

Chart of the Week: Services Market by Sector

ISG’s breakdown sector growth demonstrates how volatile industry specific services can be despite the overall market forecasting smooth growth. Service providers that can’t withstand this volatility should consider targeting several verticals that are complementary in order to hedge risk.

The overall business services sector is expected to grow in 2024, but providers must understand it won’t be smooth across verticals and should expect similar results to the chart above. In addition, providers should start thinking of which verticals may outperform in 2024 and determine whether they can expand, or break into, those markets.

About Us

Panther Equity Group is a private equity firm focused on making investments within the IT Services, Technology Services, Business Services & eCommerce verticals.

Our team and Operating Partners have decades of experience within our focus verticals along with a vast network of experienced operators and LP investors.

We have the Operational, Technology, M&A, Business Development, and industry-specific Strategy expertise to help companies accelerate their growth and reach their full potential. Learn more about Panther Equity Group by heading over to our website:

A Trusted Partner For Founders, Companies & Entrepreneurs

Industry Commentary

Digital Supply Chain

E-Commerce

📖 The Future of E-Commerce

Cloud M&A

🎤 Beyond the Dynatrace Partnership

If you’re a company Founder / Shareholder interested in working with Panther, a deal maker interested in connecting or with a deal to share, or an Operating Executive looking for a part-time, full-time, or a Board Level Role — feel free to get in touch with us!

Private Market Movements

Private Market Returns Shift Downwards

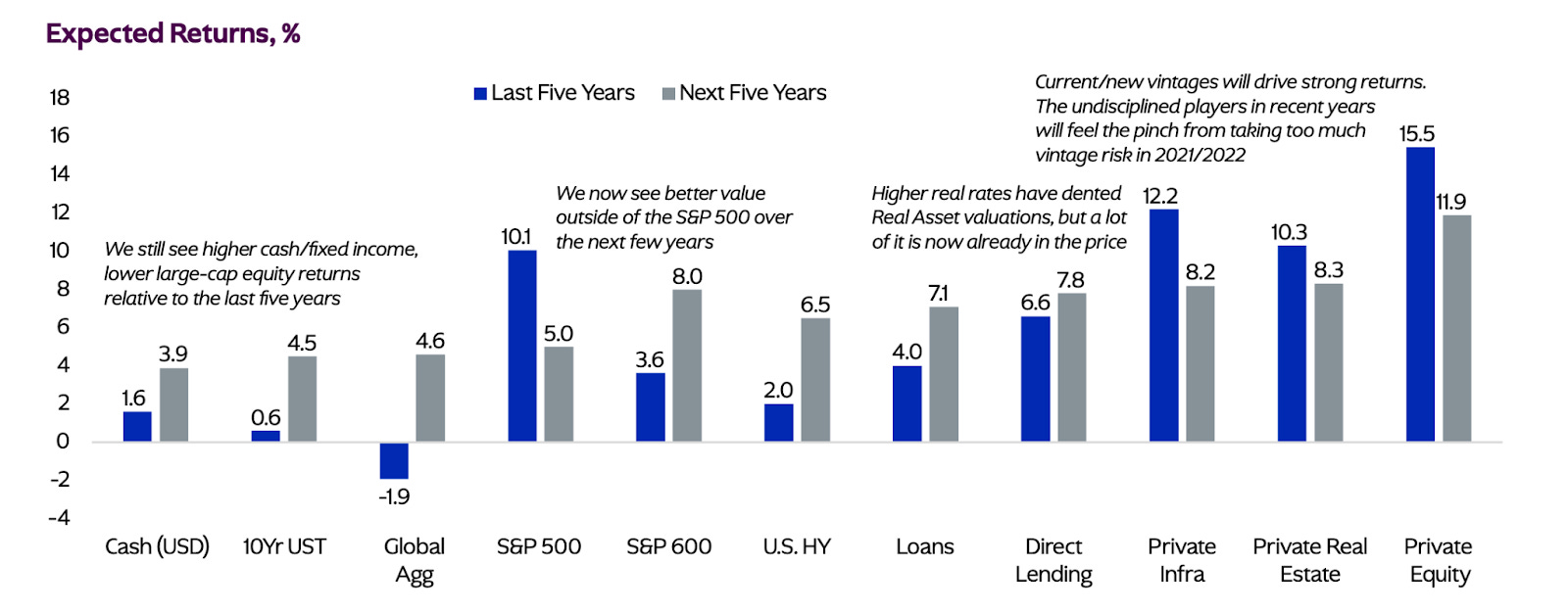

Leading private equity giant KKR’s latest report on private investments predicts a transformational 2024, as the market anticipates a transitional year with significant changes influenced by factors such as below-consensus inflation, fiscal impulse, labor costs, energy transition, and global supply chain restructuring. The focus on asset allocation strategies will be crucial in navigating these shifts.

Expected returns in private equity are projected to decrease to 11.9% over the next five years compared to the 15.5% returns of the previous five years, as seen in the chart above. However, this decline is attributed to undisciplined investments made during the frenzied years of 2021 and 2022, rather than fundamental issues in the market.

Strong returns are expected from current and new funds, with a potential drag from imprudent or rushed investments made during the years of near-zero interest rates. Private equity investors should expect similar returns from upper quartile firms going forward, but also much poorer performance from lower tier investors.

Structural Private Market Shifts Investors should Monitor

In addition to an anticipated change in expected returns, KKR’s report also highlights key structural shifts in private equity investing, with the most significant being capital structure. Equity portions of recent deals are higher and debt percentage has decreased, reducing the long-term risk of these investments.

As a result, value creation becomes more crucial than ever to offset higher rates, and this can be done through operational improvements, accretive acquisitions, and strategic changes.

Finally, exit multiples will also see a longer-term decrease, as they are correlated to rates. However, public markets have shown a willingness to pay higher multiples for companies that appear big, thematic, and simple. Investors can create value by thinking of how portfolio companies can be positioned to achieve these higher multiples.

Overall, investors should take note of these structural shifts when conducting diligence on investments or GPs. Well-managed private equity vintages, with a focus on operational improvement and disciplined capital structures, will perform better than expected in this evolving environment.

About Panther Equity Group

Panther Equity Group is a private equity sponsor seeking to provide capital, strategic support, and resources to healthy & well-positioned private companies in the lower middle market. We typically focus on companies with $2 million - $12 million in EBITDA and seek to make majority or significant minority equity investments.